Advancements in Electronic Fare Payment: Contactless and Open Loop Technologies

2021 Executive Briefing

BRIEFING HIGHLIGHTS:

- Contactless bank cards and open-loop fare payment technologies are an evolution of electronic fare payment technologies.

- COVID-19-related safety concerns have made these systems more relevant than ever, accelerating their deployment.

- These technologies can reduce system costs and improve the customer experience, but equity issues persist.

Introduction

Electronic fare payment (EFP) has long been used in the transit industry to facilitate fare collection. These systems, representing an advancement from mechanical or operator-based cash-only systems, can eliminate the need for travelers to have exact change when taking transit. They can also reduce operational costs for agencies, as cash is expensive to secure, transport, store, and count [1], [2].

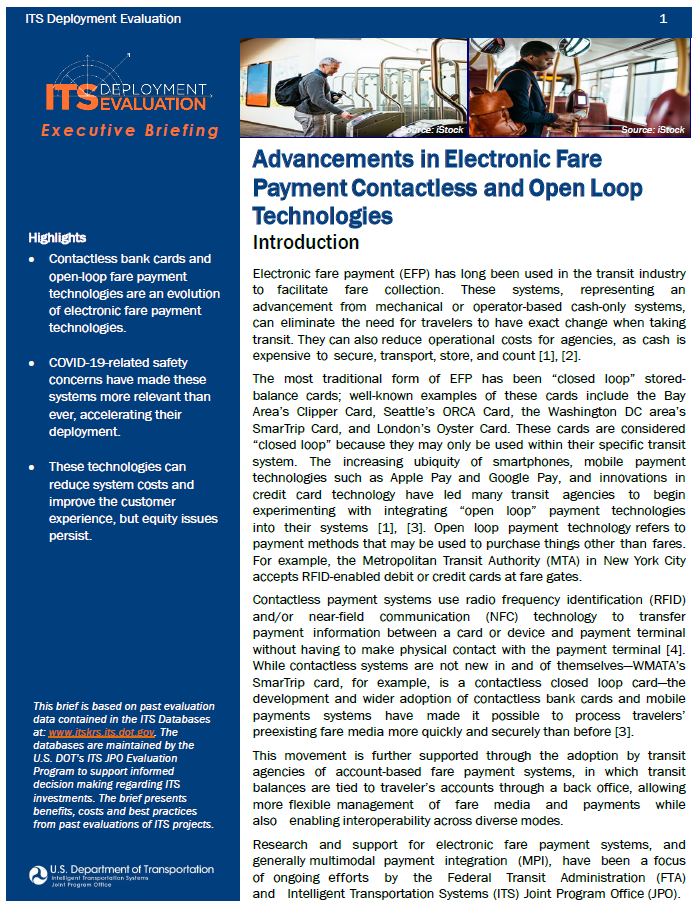

The most traditional form of EFP has been “closed loop” storedbalance cards; well-known examples of these cards include the Bay Area’s Clipper Card, Seattle’s ORCA Card, the Washington DC area’s SmarTrip Card, and London’s Oyster Card. These cards are considered “closed loop” because they may only be used within their specific transit system. The increasing ubiquity of smartphones, mobile payment technologies such as Apple Pay and Google Pay, and innovations in credit card technology have led many transit agencies to begin experimenting with integrating “open loop” payment technologies into their systems [1], [3]. Open loop payment technology refers to payment methods that may be used to purchase things other than fares. For example, the Metropolitan Transit Authority (MTA) in New York City accepts RFID-enabled debit or credit cards at fare gates.

Contactless payment systems use radio frequency identification (RFID) and/or near-field communication (NFC) technology to transfer payment information between a card or device and payment terminal without having to make physical contact with the payment terminal [4]. While contactless systems are not new in and of themselves—WMATA’s SmarTrip card, for example, is a contactless closed loop card—the development and wider adoption of contactless bank cards and mobile payments systems have made it possible to process travelers’ preexisting fare media more quickly and securely than before [3].

This movement is further supported through the adoption by transit agencies of account-based fare payment systems, in which transit balances are tied to traveler’s accounts through a back office, allowing more flexible management of fare media and payments while also enabling interoperability across diverse modes.

Research and support for electronic fare payment systems, and generally multimodal payment integration (MPI), have been a focus of ongoing efforts by the Federal Transit Administration (FTA) and Intelligent Transportation Systems (ITS) Joint Program Office (JPO).

The COVID-19 Pandemic and EFP

The adoption of contactless bank cards has generally been slow in the United States [3]. Likewise, open loop payment has taken time to roll out in transit systems across the US. This is often attributed to both technical and procurement challenges. For example, early implementations of open and contactless credit cards took more than one second to fully authenticate the transaction. While this wait time might be manageable in retail settings, it is too long a processing time for fare payment, which relies on being able to quickly and efficiently manage dozens of travelers entering and exiting a station or vehicle. Likewise, institutional factors such as long-term equipment contracts and complex fare payment rules have complicated adoption efforts [1], [3], [6].

| Open loop fare payment systems may be especially beneficial for tourists. Visitors do not need to purchase a new card or navigate potentially confusing ticketing systems to use public transit. |

However, the COVID-19 pandemic, which began in early 2020, has greatly increased interest in and support for the roll-out of contactless payment technologies, making them more relevant than ever. Throughout the pandemic, transit agencies have looked for ways to facilitate social distancing, reduce “high-touch” surfaces in systems, and allay traveler concerns about COVID-19 transmission. Many have turned to contactless payment technologies as a promising solution [3], [7]. For example, Capital Area Transit System in Baton Rouge, Louisiana is using a federal grant to roll-out contactless fare payment as part of its “COVID safe” strategy [8]. Likewise, Monterey-Salinas Transit in California is actively working to upgrade to a contactless system and views this move as a key part of its COVID response strategy [3].

Benefits

One of the primary benefits of open loop fare payment technology is its cost savings. In 2021, the Washington Metropolitan Area Transit Authority (WMATA) accelerated the rollout of its mobile payment fare technology. WMATA conservatively estimated that between fiscal year 2021 and 2029, the new payment technology will generate more than $4.4 million in savings from reducing fare collection and card provisioning costs. Overall, the shift is expected to save $3.6 million after accounting for an incentive program that will be pursued by the agency to encourage travelers to shift to payment services such as Apple Pay and Google Pay. Moreover, in addition to these savings, WMATA highlighted the benefits to health and safety from this pivot to open-loop payments, noting that they were “a top priority” for the agency (2021- 01591).

In another case, one of the early leaders in contactless openloop fare payment systems is the London Underground, also referred to as “the Tube.” Transport for London (TfL), the responsible transit authority, began accepting contactless bank cards and mobile payment systems in 2014 and 2015. By 2016, TfL estimated that these systems, in conjunction with contract restructuring, reduced the cost of fare collection from 15 percent of revenue to less than 9 percent of revenue. Due to the high throughput of the London Underground system—at the time, it was already considered to be among the largest contactless merchants in the world—this savings is significant (2021- 01590).

Costs

New York’s MTA is the largest public transit system in the United States, operating more than 470 stations and handling nearly 1.7 billion passengers each year. While it previously only accepted cash payments and its magnetic-stripe MetroCard, it recently undertook a multi-year, extensive upgrade to its fare payment system. The goal of this upgrade was to make the system fully contactless and compatible with open-loop payments. The initiative, called One Metro New York (OMNY), was launched in 2019, and began converting fare machines in each of MTA’s stations. By late 2020, installation was complete and the system was fully available across New York City. The MTA reports that the development, testing, and installation of the system cost $640 million, with costs remaining on-budget despite a six-week disruption due to the coronavirus pandemic (2021-00492).

The agency has begun to roll out an OMNY app, as well as physical OMNY cards, for users by the end of 2021 and will spend the next few years focusing on expanding fare options—introducing reduced and student fares across different modes, for example—with final completion and integration of the OMNY system expected in 2023. As of 2021, MTA is in the process of monitoring the overall benefits of implementing the OMNY system, but preliminary numbers indicate positive responses from the public. As of June 2021, the OMNY system averages 600,000 uses per day and has had nearly 17 million uses in the month of June 2021.

Best Practices

Equity Considerations The deployment of EFP systems has important equity implications, both positive and negative, and agencies have developed best practices to mitigate some of the negative equity effects of EFP deployment.

On the positive side, EFP systems can increase access to transit systems for riders who prefer to use electronic payment or who carry no cash, which is a growing percentage of Americans [10]. EFP systems also can facilitate fare policies and programs that increase transit access for marginalized groups. Traditionally, transit operators have offered fare discount programs for a variety of traveler groups, such as those with disabilities, low income travelers, veterans, older adults, and students. However, historically, these programs have been complicated to enroll in, with many programs for travelers with disabilities requiring certification by a health care professional, for example. EFP systems can greatly streamline these programs, by allowing for online or even automatic enrollment. For example, the Orange County Transit Authority automatically displays the correct type of transit pass to prequalified users in its transit app [15].

Additionally, fare capping, which limits the maximum daily, weekly, or monthly charge for travelers is only possible with the use of EFP. Many agencies view fare capping as an important step forward for transit equity as it ensures riders do not overpay and keeps costs reasonable and predictable for travelers, even encouraging greater use of transit [11]. Traditionally, low-income riders have been unable to benefit from the cost savings of weekly or monthly passes due to the high up-front cost. Fare capping allows these passes to be gradually earned, eliminating the initial barrier and ensuring greater access for travelers.

On the negative side, EFP systems may exclude travelers who are unbanked and/or underbanked. Moreover, as EFP systems become more common, methods of using cash payments are typically made more complex— for example, requiring cards to have value added to them at dedicated kiosks or retail providers, no longer letting travelers use cash directly upon boarding a vehicle. A report from the National Institute for Transportation and Communities outlines some of the best practices to mitigate these equity concerns. These strategies include:

- Fare Free Transit: Collecting fares is not free, and for smaller agencies fare collection expenses are very high compared to fare revenue. In Eugene, Oregon, for example, the transit agency expends 40 percent of its revenue to collect fares. In these situations, eliminating fare collection entirely may be a prudent financial choice.

- Simple Cash Collection: Simple, non-validating cash collection is another option to allow for cash fare collection. If the volume of cash fares is low overall, then there is no need for more expensive fare validation machines. In Eugene, Oregon cash on-board fare collection significantly boosted ridership.

- Retail service: Finally, integration with retail services is a common strategy to provide options for travelers to use cash. With retail partnerships, travelers can purchase fare media from a variety of providers, such as grocery stores, convenience stores, or public facilities such as libraries. Such partnerships are typically a convenient and low-cost strategy for transit agencies, but the specific geographic coverage of retail services can vary, and in some cases may not meet the needs of all travelers.

Case Study

The Chicago Transit Authority (CTA) is the regional transit system operating bus and heavy rail service in the Chicago, Illinois area. In 2013, CTA introduced its innovative Ventra payment system. The Ventra system is a fully integrated, electronic, regional fare system that allows users to pay for CTA, METRA (commuter rail), and PACE bus (regional/commuter bus) service.

CTA sought to integrate both open loop and contactless technology into the Ventra system from the outset. Customers may use a physical Ventra card, a mobile Ventra card integrated with Apple Pay and Google Pay, the Ventra app, or their own contactless bank cards to pay for fares. The original version of the Ventra card included debit card functionality, allowing it to be used for non-transit purchases; however, this has been phased out due to the additional associated technical difficulties and low customer utilization.

This adoption of contactless payments came as a strategic development; CTA recognized that ridership had been declining and developed the Ventra system as a means of making the fare payment process easier and more accessible to users. By providing travelers with “one-stop shopping,” CTA was able to consolidate the travel experience across multiple systems in the area. The agency noted that public support, including a legislative mandate to develop an integrated fare payment system, was crucial to the success of its development.

A 2021 report by the Chicago Metropolitan Agency for Planning (CMAP) evaluating transit equity in the region noted that the Ventra card’s capacity to be reloaded with cash compared favorably to similar transportation related costs, which were not as accessible to un- or under-banked city residents to manage. For example, transportation-related fees managed by the Illinois Secretary of State must be paid through online portals, with difficult-to-manage workarounds for unbanked users. This results in an inequity of access to payment methods, leading the report to recommend partnership with CTA and allowing such fees to be paid through Ventra cards [13]. While this recommendation is nonbinding and would still require users to have access to the internet, it emphasizes the important role that transit fare payments can play in the lives of many Americans and the opportunities offered by wider integration.

In addition to increasing riders’ access to local transit systems and thus potentially boosting ridership, the upgrade to the Ventra system allowed the agency to generate rider data to better understand its customer base and tailor its services accordingly.

Recently, CTA launched a pilot effort to further integrate Chicagoland services into the Ventra system. CTA sought to allow users to pay for the Divvy Bike Share program with Ventra. Divvy, a program initially funded by the Chicago Department of Transportation and operated by the rideshare company Lyft, has more than 650 stations across the region, many of which are close to CTA stations.

This potential for multimodal integration is the focus of CTA’s MOD Sandbox project, which came in two phases: first, to integrate bikeshare information into the Ventra app; second, to integrate bikeshare payments [14]. The project has faced several institutional and technical challenges; in particular, both the Ventra app and the Divvy bikeshare services have had changes in operators since the beginning of the effort, leading to unavoidable technical delays. The project is still preparing for launch, but the pilot team has used these challenges and their responses to them as an opportunity to develop best practices and lessons learned for other agencies that are interested in pursuing similar projects. Some of these lessons are:

- Integration requires patience. Even when stakeholders are ready, willing, and able to pursue integration, the challenge of integrating multiple technically complex systems may take time to get right.

- There can be tradeoffs between pace and efficiency. By slowing down the process of integration, CTA ensured that systems could be built from the ground up and not require redundant effort.

- Public-private partnerships can present unforeseen risks. Both the Ventra app and the Divvy service underwent changes in operators during the project, presenting a novel challenge to the system upgrade. However, the stakeholders maintained a diligent effort to ensure continuity and provide stability through the transition.

- Due diligence is important. Agencies that do not have their own in-house technical expertise on fare payment and integration may want to conduct feasibility assessments as part of the groundwork for future projects. These assessments can ensure that technical and institutional gaps may be filled without expanding the scope or budget of the project.

References

- L. Bliss, "Bloomberg CityLab," Bloomberg, 1 February 2021. [Online]. Available: https://www.bloomberg.com/news/articles/2021-02-01/covid-made-the-case-for-contactless-transitfares. [Accessed 19 August 2021].

- S. Walden, "Forbes Advisor," Forbes, 12 June 2020. [Online]. Available: https://www.forbes.com/advisor/banking/banking-after-covid-19-the-rise-of-contactless-payments-in-theu-s/. [Accessed 19 August 2021].

- USDOT, "Research & Innovation," Federal Transit Administration, 27 August 2021. [Online]. Available: https://www.transit.dot.gov/research-innovation/mobility-payment-integration-mpi-program.

- Intelligent Transportation Systems Joint Program Office, "ITS Transit Fact Sheets," 2021. [Online]. Available: https://www.pcb.its.dot.gov/factsheets/efp/efp_overview.aspx#page=tech. [Accessed 19 August 2021].

- A. Shayan, "Forbes," Forbes Finance Council, 30 July 2021. [Online]. Available: https://www.forbes.com/sites/forbesfinancecouncil/2021/07/30/whats-driving-contactless-payments-intransit---and-how-agencies-can-ensure-a-smooth-rollout/?sh=5e6b6847305f. [Accessed 20 August 2021].

- L. Yvkoff, "Forbes," Forbes, 28 April 2020. [Online]. Available: https://www.forbes.com/sites/lianeyvkoff/2020/04/28/as-commuters-eye-returning-to-work-some-citiesaccelerate-implementation-of-ticketless-public-transit/?sh=6f8e4afc7058. [Accessed 19 August 2021].

- WBRZ, "WBRZ News," WBRZ, 20 January 2021. [Online]. Available: https://www.wbrz.com/news/catsto-become-more-covid-safe-with-contactless-bus-fare-payment-system/. [Accessed 19 August 2021].

- Transport For London, "Annual Report and Statement of Accounts," Transport For London, London, 2016. Available: https://content.tfl.gov.uk/tfl-annual-report-2015-16.pdf

- J. Hollnagel and A. Fook, "The Future of Fare Media in Automated Fare Collection Systems for Urban Mobility in the Latin America and Caribbean Region," 2019. Available: https://publications.iadb.org/publications/english/document/The_Future_of_Fare_Media_in_Automated_ Fare_Collection_Systems_for_Urban_Mobility_in_the_Latin_America_and_Caribbean_Region_en.pdf

- R. Kumar and O. Shaun, "2019 Findings from the Diary of Consumer Payment Choice," Federal Reserve Bank of San Francisco, San Francisco, 2019. Available: https://www.frbsf.org/cash/publications/fed-notes/2019/june/2019-findings-from-the-diary-of-consumerpayment-choice/

- A. Stuntz, "Transit Fare Policy: Use of Automated Data to Improve Incremental Decision Making," Massachusetts Institute of Technology, 2018. Available: https://dspace.mit.edu/bitstream/handle/1721.1/119275/1065525444-MIT.pdf

- A. Golub, A. Brown, Brakewood, Candance and J. MacArthur, "Applying an Equity Lens to Automated Payment Solutions for Public Transportation," National Institute for Transportation and Communities, 2021. Available: https://nitc.trec.pdx.edu/research/project/1268/Applying_an_Equity_Lens_to_Automated_Payment_Solu tions_for_Public_Transportation

- Chicago Metropolitan Agency for Planning, "Improving equity in transportation fees, fines, and fares," Improving equity in transportation fees, fines, and fares, Chicago, 2021. Available: https://www.cmap.illinois.gov/documents/10180/1307930/FFF_final_report.pdf/1d74b660-c1c3-a2c0- dcb0-879d4493a499?t=1617741942903

- USDOT Federal Transit Administration, "Cohen, Adam; Shaheen, Susan; Broader, Jacquelyn; Martin, Elliot," Federal Transit Administration, 2021. Available: https://www.transit.dot.gov/sites/fta.dot.gov/files/2021-06/FTA-Report-No-0196.pdf

- Orange County Transportation Authority, "Mobile App," OCTA, [Online]. Available: https://www.octa.net/Bus/Fares-and-Passes/Mobile-App/.

{kind=link}